Interest-Only vs. Principal-and-Interest: The Cash Flow Battle

- Joshua Flack

- Apr 12

- 4 min read

TL;DR

In a high-rate, modest-growth market, structure matters more than ever. Interest-only (IO) lending wins on short-term cash flow, often improving holding costs by hundreds per month and reducing negative gearing pressure. Principal-and-interest (P&I) wins on long-term wealth, steadily reducing debt and interest exposure. The data shows IO can cut weekly holding costs significantly, but increases total interest paid and leaves you exposed to refinancing risk. In 2026, the “best” structure isn’t universal. If your strategy is yield, portfolio growth, and flexibility, IO often fits. If your goal is debt reduction and certainty, P&I is the safer path. Most investors should use both deliberately.

The context: why this decision matters more in 2026

The market has shifted. Debt is expensive. Capital growth is subdued. Yields have improved, but not enough to hide poor structure.

That changes the question.

It’s no longer “which loan is cheaper? ”It’s “which structure keeps you in the game long enough to win?”

Because right now, cash flow determines survival.

What the numbers say: IO vs P&I in practice

Let’s anchor this in reality.

A typical example from current NZ lending:

$700,000 loan at ~4.5–6%

P&I repayment: ~ $3,600/month

Interest-only repayment: ~ $2,600/month

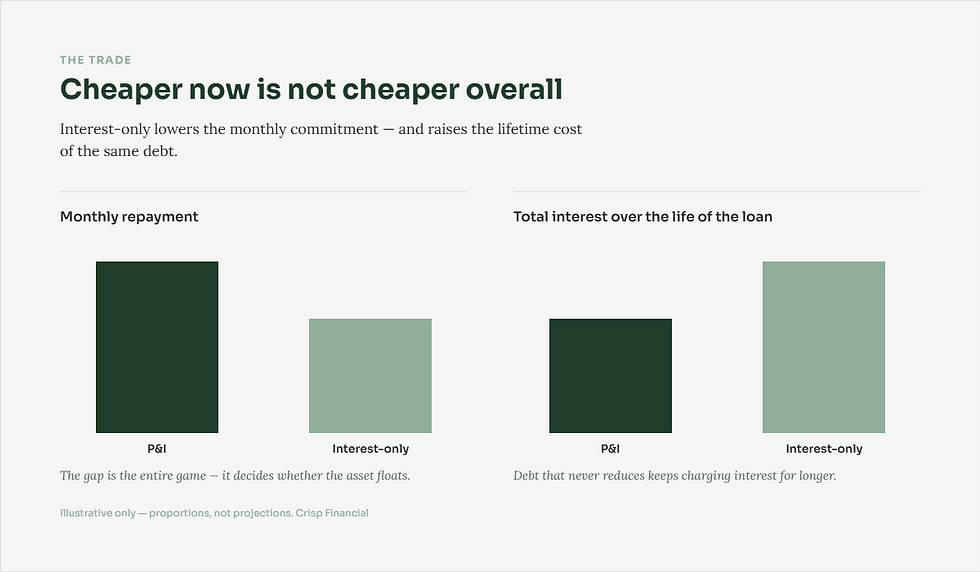

That’s roughly $1,000 per month difference.

On a rental:

P&I structure: often -$200 to -$300/week

IO structure: closer to -$50/week

That gap is the entire game.

One structure forces you to subsidise heavily.The other keeps the asset afloat.

Interest-only: the cash flow operator

IO loans are simple. You pay interest. The debt doesn’t reduce.

That’s exactly why investors use them.

What the data shows:

Lower repayments improve serviceability and portfolio scalability

Rental income is more likely to cover costs

Interest remains tax-deductible for investors in NZ

In practical terms:

You preserve cash

You reduce weekly holding costs

You buy time

This matters in a flat market. If growth is muted, you’re not being paid to carry a loss.

IO lets you hold assets without bleeding.

That’s why most portfolio investors lean this way early.

The trade-off: IO is not “cheaper”

It just feels cheaper.

Because:

You’re not reducing debt

You pay interest for longer

Total borrowing cost increases over time

A simple outcome:

5 years IO = lower payments now

But higher lifetime interest cost later

You’re effectively choosing:

Short-term survival

vs

Long-term efficiency

There’s also a structural risk.

At the end of the IO term:

repayments jump

refinancing is not guaranteed

lending criteria may tighten

If you can’t refinance or convert, you may be forced to sell.

That risk is often ignored.

Principal-and-interest: the long game

P&I is slower, but cleaner.

Every payment:

reduces debt

lowers future interest

builds equity

It’s forced discipline.

Banks prefer it for a reason.

What it does well:

De-risks over time

Improves equity position regardless of market

Removes reliance on refinancing

If the market goes sideways for 5–10 years, P&I investors still move forward.

IO investors don’t.

The real comparison: cash flow vs control

Strip it back.

Factor | Interest-Only | Principal & Interest |

Monthly cash flow | Strong | Weak |

Portfolio scalability | High | Limited |

Debt reduction | None | Consistent |

Total interest paid | Higher | Lower |

Risk at reset/refinance | Higher | Lower |

Flexibility | High | Low |

That’s the trade.

2026 reality: yield is back, but not enough

Here’s the mistake most investors make right now.

They assume higher yields fix everything.

They don’t.

Even with improved rents:

P&I still creates negative cash flow in many cases

IO often moves deals closer to neutral

That difference determines whether you can:

buy another property

hold through rate cycles

survive shocks

Structure isn’t a detail. It’s strategy.

When IO is the right move

IO works best when:

You’re in growth or accumulation phase

You want to maximise borrowing capacity

You’re managing multiple properties

Cash flow is tight or uncertain

You plan to recycle or restructure debt later

In short:

You’re playing offence.

When P&I makes more sense

P&I is better when:

You’re nearing retirement

You want certainty and simplicity

You’re holding fewer properties

You prioritise debt reduction over expansion

You don’t want refinancing risk

You’re playing defence.

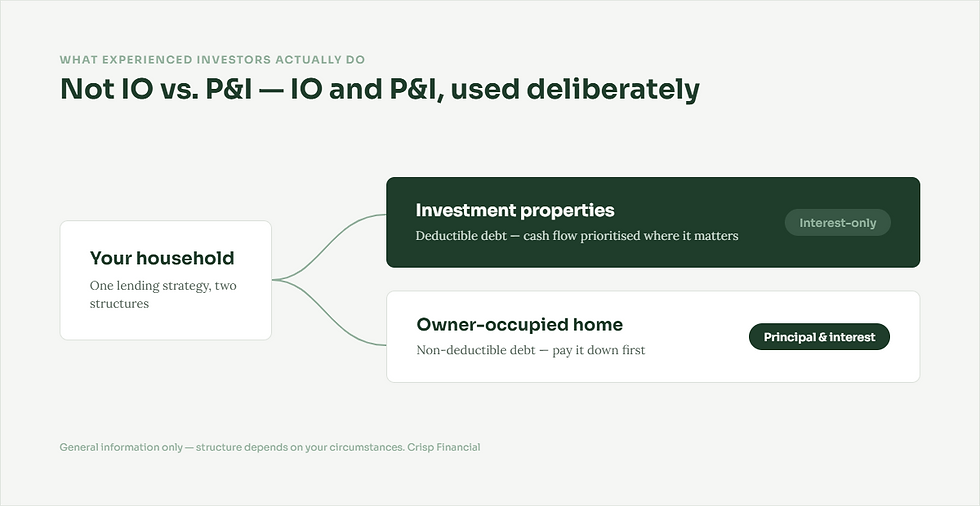

The hybrid strategy (what experienced investors actually do)

This is where most people get it wrong.

It’s not IO vs P&I.

It’s IO and P&I, used deliberately.

A common structure:

Investment properties → Interest-only

Owner-occupied home → Principal & interest

Why?

Investment debt is typically tax-deductible

Personal debt is not

Cash flow is prioritised where it matters

This approach:

improves overall household position

accelerates net worth

keeps flexibility

It’s not theory. It’s how portfolios scale.

The real risk in 2026

It’s not choosing IO.

It’s choosing IO without a plan.

Problems show up when:

investors assume growth will bail them out

they don’t prepare for P&I rollovers

they rely on refinancing in tighter credit conditions

We’ve seen this before.

If values stall or drop, IO magnifies risk because equity doesn’t move.

Bottom line

IO is a cash flow tool

P&I is a debt reduction tool

Neither is “better”.

But in a high-rate, modest-growth environment:

IO often keeps deals viable

P&I often kills scalability

The right answer depends on your phase, not your preference.

If you’re not actively choosing your loan structure, you’re leaving performance on the table.

At Crisp, we design lending structures around outcomes, not products. That means aligning cash flow, tax position, and long-term strategy from day one.

If you want a clear view on how your current or next deal should be structured, get in touch. We’ll map it properly before you commit.

Relevant tools and resources available for free here:

Other relevant articles to check out:

About the Author:

Joshua Flack is a mortgage and lending adviser and the founder of Crisp Financial. Before finance, he spent two decades running businesses across construction, facilities services, and franchising, which is why his advice starts with how the numbers actually work rather than how the brochure says they should. He works with home buyers, investors, and self-employed borrowers across New Zealand, with particular depth in complex and non-standard lending. Crisp Financial Limited (FSP1012114) operates under the Link Financial Group FAP licence. The information in this article is general in nature and is not regulated financial advice.

Comments